This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

LE analysts report that the upper-midscale chain scale continues to have the largest project count in the U.S. The upscale chain scale follows with 1,407 projects/174,127 rooms. Together, these two chain scales comprise 60% of all projects in the total pipeline. supply increase. supply increase.

Throughout these three regions, upscale and upper midscale chain scale projects continue to dominate the pipeline, accounting for 4,240 projects/492,591 rooms, or 67% of the projects and 64% of the rooms in the construction pipeline. Certainly, these two chain scales will have the most new hotel openings through 2025.

The solution brings IDeaS robust demand forecast and price sensitivity capabilities together to help hoteliers allocate marketing spend for the greatest impact on incremental revenue. Powered by IDeaS G3 RMS advanced forecasting engine, Spotlight enables teams to proactively adjust strategies and take a surgical approach to demand generation.

The upper-upscale, upscale and upper-midscale chain scales account for 61% of projects and 64% of the rooms in the pipeline. Projects in the upscale chain scale dominate the APEC pipeline at Q3 with 510 projects and 101,067 rooms, both reaching all-time highs.

At Q1, the luxury chain scale reached a record high of 132 projects/17,124 rooms, while the upper-upscale chain scale also hit a record high with 281 projects/45,091 rooms. The upscale chain scale stands at 358 projects/55,297 rooms, while the upper-midscale chain scale closed the first quarter with 325 projects/47,738 rooms.

“The reintroduction of the much-loved Rendezvous brand into New Zealand – through the Rendezvous Heritage Christchurch and Rendezvous Heritage Queenstown – provides Asia Pacific scale to the portfolio and will see TFE venture into Otago for the first time.” million in the July 2024 year, an increase of 604,000 from the July 2023 year.

LE analysts report that the upper-midscale chain scale stands at 2,262 projects/219,547 rooms and has the largest project count of all chain scales in the total construction pipeline at Q2. The second largest is the upscale chain scale, which has 1,417 projects/175,343 rooms. growth, respectively. equating to a 1.8%

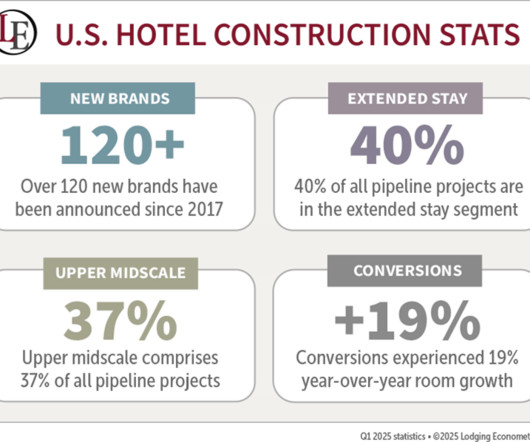

hotel construction pipeline is being driven in large part by the introduction of more than 120 new brands since 2017 and focused development in two high-performing segments: the upper-midscale chain scale and extended-stay accommodations. The expansion of the U.S. This anticipated total of 740 new hotels (83,548 rooms) represents a 1.5%

The upper-midscale chain scale continues to lead Chinas hotel construction pipeline at the close of the first quarter with 1,161 projects/177,644 rooms. Upscale chain scale projects in China reached an all-time high project total at Q1, standing at 1,043 projects/223,499 rooms, up 11% by projects YOY and 5% by rooms YOY.

By chain scale, LE analysts report several record highs reached in Q1 2025. The luxury chain scale achieved all-time high totals with 185 projects/42,268 rooms, while the upper-upscale chain scale reached record highs with 153 projects/37,946 rooms. During the first quarter, the Middle East opened 9 new hotels/2,130 rooms.

One of the main challenges for hotels is creating accurate forecasts in the short, medium, and long term. Accurate forecasting also benefits hotels’ bottom lines in other ways. But traditional forecasting models no longer cut it. Relying on historical data hinders performance since no season is ever identical to the last.

By chain scale, upper-midscale hotels dominate with 132 projects/14,039 rooms, representing 40% of the total projects and 32% of rooms in the pipeline. LE is forecasting 43 new hotels/5,321 rooms to open in 2025, representing continued growth in supply. Through Q4 2024, Canada opened 15 new hotels with 1,478 rooms.

The upper-midscale segment is the preferred chain scale for development at Q4 close with 1,215 projects/185,100 rooms, accounting for 32% of the projects in Chinas total pipeline. Together with the midscale chain scale’s 411 projects/40,661 rooms, these three chain scales account for 70% of all projects in China’s pipeline.

This disproportionate growth between project count and room numbers suggests a trend toward smaller-scale developments. By chain scale, upper-midscale hotels lead the pipeline with record numbers: 135 projects (14,219 rooms), representing 41% of total projects and 35% of rooms.

By analyzing real-time market data, booking patterns, and competitor pricing, AI-powered systems can automatically adjust room rates, forecast demand, and allocate inventory across channels more effectively than any human team. Today, AI has flipped that model on its head.

The higher-end chain scales continue to dominate the APEC regions pipeline at the Q4 2024 close by projects. In total, these three chain scales account for 1,261 projects totaling 260,178 rooms, or 60% of projects and 63% of rooms in APECs pipeline. Upper-upscale projects also grew slightly YOY at Q4 with 368 projects/80,095 rooms.

Executives from CoStar, CBRE, Kalibri Labs and more forecast how hotels will perform this year, while owners and operators provide their thoughts on how each chain scale will do. The 2024 U.S. Industry Outlook originally ran as a supplement to the January 2024 issue of Hotel Business. Complete the form below to download the report.

The record-high project and room counts in the total pipeline can be attributed to the continued growth of the upscale and upper-midscale chain scales, both of which hit record highs this quarter. The upscale chain scale ended Q3 with 1,026 projects/224,688 rooms, up 14% by projects and 9% by rooms YOY.

CBRE is forecasting RevPAR growth to recover in 2024 as inbound international travel further improves and sector-specific headwinds moderate. The company forecasts 3.0% CBRE’s baseline forecast anticipates 0.8% CBRE’s baseline forecast anticipates 0.8% ADR increase. average GDP growth and 2.9% average inflation in 2024.

IHG forecasts that 70% of Crowne Plazas Americas estate will showcase updated designs by the end of 2025. Crowne Plaza Louisville Airport Expo Center recently finalized a full-scale renovation under the direction of owner Al J. The property owned and managed by National Hospitality Services. Schneider Company.

Seventy-two percent of its pipeline is concentrated in the three highest chainscales: luxury, upper-upscale and upscale, which typically boasts larger scale projects. LE is forecasting 26 additional new hotel openings with 4,434 rooms by year-end. Of note, Wynn Resorts will open a new hotel on the island of Ras Al Khaimah.

Move Beyond Syncing, Start Scaling 1) The New Age of Hotel Distribution The hotel distribution landscape has changed. Identify high-performing channels, forecast demand, monitor acquisition cost per booking, and refine your strategy in real time. Multi-Property and Group Benefits 6. Leveraging Data for Smarter Distribution 7.

Growth rates are subdued across the region driven by weaker than forecast inbound tourism and persistent levels of inflation and interest rates. As market consolidation continues to rise, owners and operators appreciate the benefits of scale and are increasingly looking to grow their portfolios.

Business Intelligence Agents: Forecasting with Real-Time and Historical Data Hotel forecasting has historically relied on manual reporting, static historical data, and siloed systems. AI-powered business intelligence agents now allow operators to synthesize data from the PMS, revenue management systems, and market sources in real time.

The luxury, upper-upscale and upscale chain scales each hit peak project counts at the end of Q4. The LE forecast for new hotel openings expects 370 new hotels/72,441 rooms to open in 2023 and 400 new hotels with 77,524 rooms forecast to open in 2024.

By chain scale, upper-midscale projects account for the largest percentage of the pipeline with 132 projects/13,870 rooms, representing 39% of the total projects. LE analysts forecast new hotel openings in Canada will continue to rise through year-end 2026 with 43 new hotel openings with 5,479 rooms.

The portfolio of solutions provides full-service, mid-scale, and limited-service hotels a range of connectivity options for delivering customized guest Wi-Fi experiences that meet the unique demands of each market segmentâfrom luxury to budget hotels. Clap resides in Connecticut with his wife and has two adult children.

An RMS should provide detailed insights into key performance metrics such as Room Revenue Per Available Room (RevPAR), Average Daily Rate (ADR), occupancy rates, booking pace, and revenue forecasts. Forecasting Accuracy: Accurate demand forecasting is crucial for anticipating future demand trends and adjusting pricing strategies accordingly.

The portfolio of solutions provides full-service, mid-scale, and limited-service hotels a range of connectivity options for delivering customized guest Wi-Fi experiences that meet the unique demands of each market segmentâfrom luxury to budget hotels. Clap resides in Connecticut with his wife and has two adult children.

The report also provides insights into the regional hotel pipeline by chain scale segment. The upscale (134 projects/18,592 rooms), luxury (121 projects/24,924 rooms and upper-upscale (104 projects/21,300 rooms) chain scales emerged with the largest pipelines.

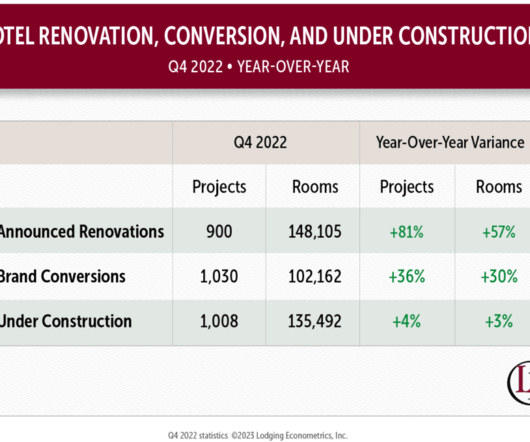

Accounting for 35% of the projects and 29% of the rooms in the combined renovation and conversion pipeline, the upper-midscale chain scale leads the way with the most activity. The upper-midscale chain scale also has the largest amount of construction activity in the U.S. with 2,175 projects/219,005 rooms.

LE analysts forecast a total of 2,531 new hotels with 380,515 rooms to open in 2023. In 2024, new openings are forecast to reach 2,674 hotels, accounting for 415,699 rooms. For 2025, LE analysts forecast 2,701 new hotels/429,006 rooms to open around the world.

Ramzy Fenianos The outlook for investment in Australasia is forecast to be relatively modest for the year ahead (2.9%), which is likely to result in significant challenges for hotel developers in the region. This trend is likely to stay as independent owners continue to navigate operating in the post-pandemic era.

The top three chain scales by total projects at the end of Q1 are upscale at 1,443 projects/179,295 rooms, upper-midscale at 2,338 projects/226,349 rooms and midscale at 974 projects/82,094 rooms. These three chain scales account for approximately 75% of the projects in the total U.S. growth rate.

Standout chain scale segments in the APEC region at the Q1 close include the upscale chain scale with a new record-high room total of 519 projects/103,815 rooms, up 9% by both projects and rooms YOY. These top two chain scales combined account for 44% of projects and 46% of rooms in the region’s total pipeline.

Predictive Demand Forecasting Predictive analytics utilizes historical data, market trends, and external factors to forecast future demand. Maintenance Forecasting : Use occupancy trends to schedule preventive maintenance before peak dates, avoiding unexpected breakdowns. Also Read: Is Your Hotel Ready for the Peak Season?

As we look ahead, LE’s report offers a detailed forecast of the anticipated supply growth. Hotel projects within the upscale and upper-midscale chain scales are leading the way. These two chain scales combined account for a substantial majority of projects. hotel landscape.

At Hotel Effectiveness, he scaled the labor optimization business by more than 500% in his tenure, where he oversaw sales, marketing and customer success. He has experience building secure systems across the entire software development lifecycle, designing patented data applications and managing large-scale distributed teams.

Therefore, if you’re not empathetic in other aspects of your life, learning to sell isn’t going to move you up the empathy scale. Unempathetic sales people can’t forecast. Empathy isn’t a trait used only for selling. It’s a life skill. Selling is about change. Unempathetic sales people rush the sale.

Standout chain scale segments in the APEC region at the Q1 close include the upscale chain scale with a new record-high room total of 519 projects/103,815 rooms, up 9% by both projects and rooms YOY. These top two chain scales combined account for 44% of projects and 46% of rooms in the region’s total pipeline.

The record-high projects in the total pipeline can be attributed to the number of upscale and upper-midscale chain scale projects, which both hit project and room-count peaks this quarter. The upscale chain scale ended Q3 with a total of 850 projects/198,277 rooms, and the upper-midscale chain scale has 1,222 projects/194,515 rooms.

At Q2, three chain scales account for an impressive 69% of the projects and 65% of the rooms in China’s total pipeline. Hotel construction projects in the upscale chain scale also reached new all-time highs at Q2, with 979 projects/219,104 rooms.

At Q2, most pipeline projects in Europe are concentrated in the upper-upscale, upscale and upper-midscale chain scales. The upscale chain scale leads with 358 projects/55,936 rooms, accounting for 21% of the pipeline. The upper-midscale segment follows closely with 335 projects/50,566 rooms, representing 20% of the pipeline.

At the Q1 close, 62% of projects in the total pipeline are concentrated within the upscale and upper-midscale chain scales. These two chain scales continue to dominate the pipeline and that is not expected to change anytime soon. Renovation and brand conversion activity in the U.S. in the first quarter. supply growth rate in 2023.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content